Economists often refer to the U.S. trade deficit and the federal budget deficit as problems of inadequate domestic saving. They speak of these deficits “crowding out” domestic investment. They allude to unspecified relationships between these deficits but seldom explain them, confusing everyone.

What is often left unsaid is that the trade deficit (when more goods and services are imported than exported), the budget deficit (when government spends more than its tax revenues), and the balance between domestic saving and investment are related to each other. In fact, their sum must equal zero. A change in any of them affects all of them. For example, tax incentives to encourage saving would likely stimulate investment, lower both the budget and trade deficits, and also reduce reliance on foreign capital. Think of three fat men filling up a telephone booth. When one inhales, the other(s) must exhale.

An Economy without Government or International Trade. To understand the interdependence of these three imbalances, first consider saving and investment in an economy with no external trade and no government. All saving (income minus consumption) and investment (output not consumed) are domestic. With different people doing the saving and investing, plans for each are likely to differ. If so, market forces — such as interest rates, prices and nominal income — will adjust until actual saving and investment balance. In this closed economy, if planned saving exceeds investment, incentives for saving (that is, interest rates) will tend to fall until saving and investment balance. Likewise, if planned investment is greater than saving, they will be brought into balance by market forces, if the economy is at or near full employment.

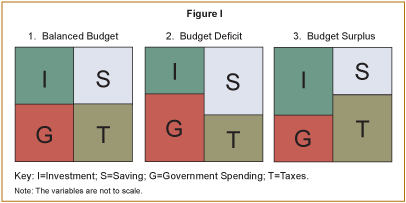

Think of saving as a leakage from the income stream which, other things equal, tends to shrink income. Think of investment as an injection into the income stream (in addition to consumption); other things equal, it tends to increase income. Income and other variables will adjust until the leakage of saving matches the injection of investment (I = S), as shown in the top half of Box 1 in Figure I.

An Economy with Government. Introducing government into the equation creates another leakage similar to saving in its impact; that leakage is taxes (T). There is also another injection into the income stream in addition to investment: government spending (G). If taxes and government spending balance — that is, if the budget is balanced (G = T) — the net impact of government on income is neutral, and private saving and investment will also balance.

An Economy with Government. Introducing government into the equation creates another leakage similar to saving in its impact; that leakage is taxes (T). There is also another injection into the income stream in addition to investment: government spending (G). If taxes and government spending balance — that is, if the budget is balanced (G = T) — the net impact of government on income is neutral, and private saving and investment will also balance.

The leakages balance the injections, but the individual components aren't necessarily equal. If government runs a budget deficit (Box 2), it will be matched by an equal surplus of private savings compared to investment (S >I). This is how a budget deficit crowds out private investment, by competing with private borrowers for savings. A budget surplus (Box 3) will be matched by an equal deficit in saving compared to investment (S < I).

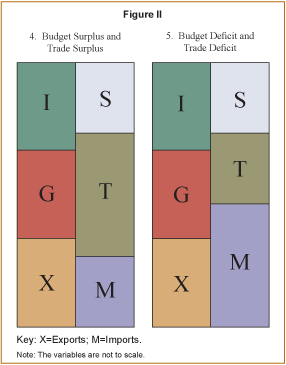

An Economy with Government and International Trade. Now, add international trade to the analysis. When we do, payments for imports become a third leakage from the domestic income stream while income from exports become a third injection. An imbalance in any of the three pairs will be matched by an opposite imbalance in the other two taken together. The principle is the same as in previous examples, but the interactions become more complex.

As shown in Box 4 (Figure II), any excess of investment over saving (I > S) is matched by a combination of budget and export surpluses (G < T and X > M). The budget surplus is positive government saving, and capital flows out to be invested abroad. This economy is sacrificing some consumption today for greater prosperity tomorrow.

The U.S. Deficits. Box 5 (not drawn to scale), depicts the current situation in the United States: The shortage of private savings (I > S) to finance domestic investment is exacerbated by negative government saving (the budget deficit, G > T). However, both these shortfalls are met by the trade deficit — or, more precisely, the inflow of foreign investment that finances the trade deficit. In other words, the United States is relying on foreign savings to supplement domestic savings. The U.S. economy consumes more goods and services than it produces thanks to foreign credit. One result is that each year's external deficit adds that amount to net foreign holdings of U.S. dollar assets. This is not necessarily a bad thing. Foreign investment has historically played an integral part in U.S. economic growth and shows that America is attractive to investors. In addition, external investment mitigates the crowd-out effect of government borrowing by expanding the pool of available credit.

The U.S. Deficits. Box 5 (not drawn to scale), depicts the current situation in the United States: The shortage of private savings (I > S) to finance domestic investment is exacerbated by negative government saving (the budget deficit, G > T). However, both these shortfalls are met by the trade deficit — or, more precisely, the inflow of foreign investment that finances the trade deficit. In other words, the United States is relying on foreign savings to supplement domestic savings. The U.S. economy consumes more goods and services than it produces thanks to foreign credit. One result is that each year's external deficit adds that amount to net foreign holdings of U.S. dollar assets. This is not necessarily a bad thing. Foreign investment has historically played an integral part in U.S. economic growth and shows that America is attractive to investors. In addition, external investment mitigates the crowd-out effect of government borrowing by expanding the pool of available credit.

The situation can become unsustainable, however, because foreign investment is funding increasing government budget deficits (government dissaving) and inadequate private saving. The growth in foreign claims on the U.S. dollar relative to U.S. claims abroad makes the U.S. economy vulnerable to the actions of foreign central banks and, possibly, sovereign wealth funds. Better to reduce that vulnerability sooner rather than have to go cold turkey later.

Reducing the Deficits. What are the policy implications of these interdependent imbalances? Here are three:

- Tax incentives to encourage saving would likely also stimulate investment and lower both the budget deficit and the trade deficit.

- Reducing the budget deficit would reduce the vulnerability of the U.S. economy to foreign creditors; rising deficits could lead to foreigners dumping dollar assets, causing equities to decline, interest rates to spike and the dollar to plunge.

- Reducing the budget deficit doesn't necessarily mean higher tax rates; marginal rate cuts reinforced by slower government spending growth would be ideal incentives.

Unfortunately, the recent tax “rebates” designed to stimulate the economy dealt a setback to budget discipline. Most people probably understand that. What they probably don't understand is that the increased budget deficit will also tend to worsen our international balance of payments and weaken the dollar. The hip bone is connected to the thigh bone; so policymakers need to study these interconnected deficits. They need to borrow my boxes.

Bob McTeer is a distinguished fellow with the National Center for Policy Analysis.