Since January 2008, 401(k) account balances have dropped up to 25 percent, on average, leaving millions of workers and retirees worried about the future of their retirement savings. Congress and President-elect Obama are considering changes to 401(k)s and other retirement accounts in response to the market turmoil. Which proposals are good ideas to improve retirement savings, and which would make matters worse?

Good Idea: Lift Mandatory Distribution Requirements on Tax-Deferred Retirement Accounts. Tax-deferred accounts include 401(k) plans offered through employers and Individual Retirement Accounts (IRAs) for the self-employed. These accounts allow individuals to invest pretax dollars that, with accumulated interest, are taxed when they are withdrawn during retirement. But they are subject to mandatory distribution rules.

The Internal Revenue Service requires seniors to begin withdrawing a minimum amount from such accounts by April 1 following the year they turn 70-and-one-half. The amount they must withdraw is determined by a formula based on life expectancy. For instance:

- A 70-and-one-half-year-old senior is required to withdraw about 3.5 percent of the total account balance.

- At age 90, however, he would be required to withdraw about 9 percent.

The percentage that seniors are required to withdraw increases because it is assumed they have fewer years to live and will need less money for future expenditures. The withdrawal amount is based on their retirement account balance as of December 31 of the previous year. But the stock market has experienced a significant drop since the end of last year. An individual invested in stocks who made a withdrawal from his account on March 31, 2008, based on the December 31, 2007 balance, had to withdraw a greater percentage of the March 31 balance, leaving less money to accrue interest in future years. Over time, the amount of accrued savings lost by seniors mounts.

President-elect Obama supports suspending the mandatory distribution requirement for at least the next two years. But an even better improvement would be to permanently change withdrawal requirements. This can be done by:

- Raising the mandatory withdrawal age; several years ago, the House Ways and Means Committee recommended raising the minimum distribution age to 75.

- Allowing seniors to withdraw from their accounts based on the average balance on their last quarterly statement, not the ending balance of the previous year.

Good Idea: New Reporting and Disclosure Rules on Retirement Account Fees. Retirement savings plans allow workers to invest in a variety of funds, including mutual stock and bond funds. Currently an employer must disclose (or provide on request) any fees charged by the funds offered to the employees, or make those fees available upon request.

However, the current disclosure rules pertaining to information from the fund managers to the employer are vague. Rep. George Miller (D-Calif.), chairman of the House Education and Labor Committee, has proposed legislation requiring funds to disclose additional fees to the employer, as well as conflicts of interest between the fund manager and the employer due to a financial or personal relationship. Employers would then be required to disclose these fees to plan participants.

Rep. Miller would also require employers to provide at least one low-cost, index fund investment option to ensure that employees have at least one reasonably safe and low-cost investment choice. However:

- Mandating an index fund option sends the message that these funds are safe since they incur lower costs than actively managed funds; but not all index funds are alike and some have performed no better than regular mutual funds.

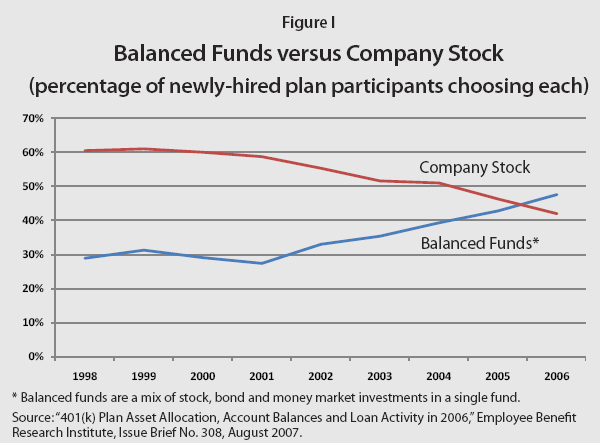

- 401(k) plans already offer an average of 14 different funds, and, moreover, new employees are increasingly choosing more stable balanced funds (a mix of stocks, bonds and money markets in one fund) over riskier investments, such as company stock. [See the Figure.]

Bad Idea: Eliminating Tax-Deferred 401(k) Plans. 401(k) plans cost the government an estimated $80 billion in tax revenues each year, and most of the breaks go to wealthier participants. This has led to calls for a redistribution of tax benefits.

At a hearing before the Rep. Miller's committee, Teresa Ghilarducci of the New School for Social Research proposed a plan to let workers trade their current 401(k) plans in for a Guaranteed Retirement Account (GRA). GRAs would essentially replace 401(k)s. Furthermore, Ghilarducci's plan would:

- Require every worker to contribute a mandatory 5 percent of after-tax earnings into a GRA (the employer would contribute half of the 5 percent).

- The government would deposit $600 a year, inflation-indexed, into the account of every worker.

- Pay a monthly amount at retirement, similar to an inflation-indexed annuity, with a guaranteed 3 percent real rate of return on the account balance.

Tax-exempt retirement accounts would be eliminated. As a result, the marginal tax rate on saving would be increased, especially for higher-income households. This would create a disincentive to save, reducing capital formation. Furthermore, GRAs are far from personal accounts:

- They do not allow individuals to pick from an array of funds; the money would instead be pooled and invested by the government as it sees fit.

- The government would have the right to reduce the guaranteed rate of return during economic down times and allow workers to access their funds during those times.

- The fund would be managed by an independent body, similar to the Thrift Savings Plan for federal employees, but Congress has frequently attempted to require the TSP to invest in funds of dubious value.

Good Idea: Expand the Saver's Credit. The Saver's Credit is a tax credit for lower- and middle-income households which allows those with 401(k)s or IRAs to receive a 50 percent matching contribution from the federal government of up to $2,000 per household. For instance:

- A married household filing jointly with an adjusted gross income of less than $31,000 would receive $2,000 for contributing $4,000 to an IRA.

- A single household with an adjusted gross income of less than $15,500 would also receive $1,000 for contributing $4,000 to an IRA.

However, the Saver's Credit is nonrefundable, which means that if a household owes no income taxes, they will not receive the credit. The solution? Make the credit refundable, so that even if a qualified household owes no income taxes, they still receive a federal match. President-elect Obama has, in fact, indicated he supports making Saver's Credit refundable.

Conclusion. A panicked reaction to the market should not take the place of common sense when it retirement accounts. Altering the mandatory withdrawal rules for seniors is wise, but scrapping the advantages of 401(k) accounts for workers is not. In the midst of the stock market chaos, let's keep the long-term outlook in perspective.

Pamela Villarreal is a senior policy analyst with the National Center for Policy Analysis.