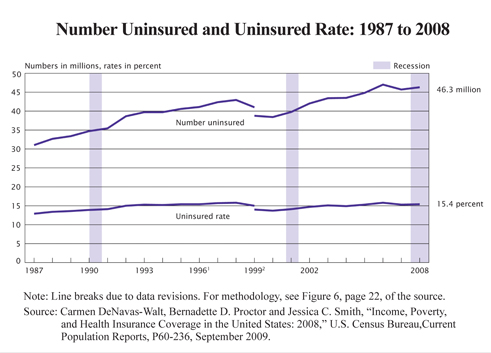

One of the primary goals of health reform is to ensure that all Americans have health insurance. Yet it is generally overlooked that the proportion of Americans without health coverage has been relatively stable over time. According to the Census Bureau, in 2008 the number of individuals in the United States lacking health coverage rose from 45.7 million to 46.3 million. The proportion of uninsured Americans remained virtually unchanged, rising from 15.3 percent to 15.4 percent.

In fact, the proportion of people without health insurance in 2008 is virtually unchanged from a decade earlier.The increase in the number of uninsured over the past decade is largely due to immigration and population growth – and to individual choice. [See the figure.]

In fact, the proportion of people without health insurance in 2008 is virtually unchanged from a decade earlier.The increase in the number of uninsured over the past decade is largely due to immigration and population growth – and to individual choice. [See the figure.]

How Big Is the Problem? In 2008, according to Census Bureau data:

- Nearly 85 percent of U.S. residents (255.1 million people) were privately insured or enrolled in a government health program, such as Medicare, Medicaid or the State Children's Health Insurance Programs (S-CHIP).

- About 13.7 million uninsured adults and children live in households earning less than $25,000 annually. Many in this group already qualify for Medicaid or S-CHIP. For instance, past research by the BlueCross BlueShield Association estimated that up to 14 million uninsured individuals qualify for public coverage but have not enrolled. Indeed, three million to six million people identified as uninsured may already be covered by Medicaid or S-CHIP but erroneously told Census Bureau they were uninsured because they do not associate Medicaid with insurance coverage. This is referred to as the "Medicaid undercount."

- Nearly 18 million of the uninsured lived in households with annual incomes above $50,000 – over half of them (9.7 million) in households with incomes that exceed $75,000 annually. There is considerable disagreement about the exact number of people in this group that may be able to afford health coverage. For instance, household income isn't the same as family income. Unrelated individual living together may not pool resources the same way families would. Yet, it is increasingly common for couples to cohabitate in lieu of marriage and function as a family unit. Arguably, many in this group could afford some type of health insurance – possibly a high-deductible plan or a plan with limited benefits.

- Nearly 15 million uninsured residents live in households with incomes of $25,000 to $50,000 per year. This group does not qualify for Medicaid and (arguably) earns too little to easily afford expensive family plans costing more than $12,000 per year. These are precisely the people who would benefit from a uniform tax credit – which has been proposed as a way to cover the uninsured.

How Serious Is the Problem? During the past 10 years the number of people with health coverage rose nearly 24 million, while the number without health coverage only increased about 3.75 million. Both increases are largely due to population growth. Typically, those who lack insurance are uninsured for only a short period of time – more than half will have coverage within a year.

Who Are the Uninsured? It is often assumed that the uninsured are all low-income families. But among households earning less than $25,000, the number of uninsured actually fell by about 12 percent over the past 10 years. The uninsured include diverse groups, each uninsured for a different reason:

Immigrants. About 12.3 million foreign-born residents lack health coverage – accounting for 27 percent of the uninsured. In 2008, nearly 45 percent of foreign-born noncitizen residents were uninsured. Income may be a factor – but not the only one. A partial explanation for this disparity is that many immigrants come from cultures without a strong history of paying premiums for private health insurance. In addition, only immigrants who have been legal residents for more than five years qualify for public coverage.

The Young and Healthy. About 19 million 18-to-34-year olds are uninsured. Most of them are healthy and know they can pay incidental expenses out of pocket. Using hard-earned dollars to pay for health care they don't expect to need is a low priority for them.

Why the Nonpoor Are Uninsured: State Mandates. Government policies that drive up the cost of private health insurance may partly explain why millions of people forgo coverage. Many states try to make it easy for a person to obtain insurance after becoming sick by requiring insurance companies to offer immediate coverage for pre-existing conditions with no waiting period. Thus, when people are healthy they have little incentive to participate and tend to avoid paying for coverage until they need care.

How to Reduce the Number of Uninsured: Uniform Tax Credit. According to the Lewin Group, a private health-care consulting firm, families earning more than $100,000 a year get four times as much tax relief as families earning $25,000. In other words, the biggest subsidy goes to those who least need it, and who probably would have purchased insurance anyway. With a uniform tax credit, low- and moderate-income families would get as much tax relief as the wealthy when they purchase health insurance.

How to Increase the Number of Insured: Allow Competition. A bill introduced by Arizona Rep. John Shadegg (R), called the Health Care Choice Act, would allow the residents of any state to purchase lower cost health insurance sold in other states. This would make coverage more affordable by injecting competition into the local market and by allowing residents to purchase insurance without expensive mandates. Consumers could shop for individual insurance on the Internet, over the telephone or through a local agent. The policies would be regulated by the insurer's home state. Consumers would be more likely to find a policy that fits their budget – giving more people access to affordable insurance. Moreover, competition across state lines would encourage state lawmakers to reduce costly insurance regulations. Economist Steve Parente and his colleagues at the University of Minnesota estimate that this change would insure an additional 12 million people.

Conclusion. Although the proportion of people without insurance coverage has changed little in recent years, much can be done to reduce the number of uninsured. This could also include a uniform tax credit like the one that has been proposed in the Patients' Choice Act of 2009, sponsored by Senator Tom Coburn and Representative Paul Ryan.

Devon Herrick, Ph.D., is a senior fellow with the National Center for Policy Analysis.